Tackling precarious work through financial regulation and private debt relief

The cost of living crisis initiated by the COVID-19 pandemic and the ongoing energy crisis has pushed firms and households to borrow significant amounts of money to meet their everyday needs. Yet, this is not a one-off event.

At least since the early 1980s, financial deregulation has allowed financial institutions to provide credit to non-financial corporations and households whose income is declining. Thus, financial commitments for both have been increasing dramatically and private debt levels have become unsustainable. At the same time, both private and public pension funds have been investing heavily in risky, high-return financial instruments and assets, risking the pension contributions of millions of current and future pensioners.

Our research suggests that personal financial insecurity and the related fear of default make workers more likely to accept working under precarious contracts, rather than negotiating for better working conditions. Using secondary data from the OECD database, we show that household debt and financial investments by pension funds increase involuntary part-time and temporary work in 22 advanced and developing economies since 1990. Therefore, this policy briefing discusses why the regulation of the financial system is an essential step towards a less precarious and more efficient labour market. Below, we offer relevant insights for policymakers and businesses.

Policy implications

• Since external financial constraints matter both for workers and firms, OECD governments should introduce private debt relief measures, on top of centralising employer-employee bargaining and empowering unions.

• Governments need to move towards pay-as-you-go pension fund models and ensure their sustainability via higher wages and prioritizing full employment.

• Businesses need to move away from employing workers under involuntary part-time and temporary contracts as a means of improving their balance sheets.

• Businesses need to invest in secure employment contracts with good working conditions and pay that allows employees to commit to their work and be more productive.

Key findings

• At least since the early 1990s, the financial system has shifted its focus to providing credit to (low-income) households and facilitating the engagement of pension funds in risky financial investments.

• The rise in private indebtedness has dramatically increased debt repayments both for non-financial corporations and households whose main priority has become to finance these payments and avoid defaulting on their debt.

• As regards non-financial corporations, the deterioration of their balance sheets due to rapidly increasing financial payments induces managers to seek ways to reduce labour costs and improve financial performance. Promoting workforce casualisation is a common approach in such cases.

• Concerning employees, first, rising financial commitments push them to take on additional precarious jobs to secure more income. Second, increased debt commitments also incentivise them to comply with managerial pressures towards casualisation for the fear of losing their job and defaulting on their debt.

• In addition, the risky financial investments of pension funds have put additional pressure on employees whose future income is in danger as a result of these investments. Consequently, younger employees may seek second jobs to earn additional income for their retirement and older employees may return to the labour market if their pension has become insufficient.

• Overall, our research provides robust statistical evidence that household debt and the risky investment of pension funds have increased involuntary atypical work, particularly involuntary part-time work, in a wide range of advanced and emerging economies since the mid-1990s.

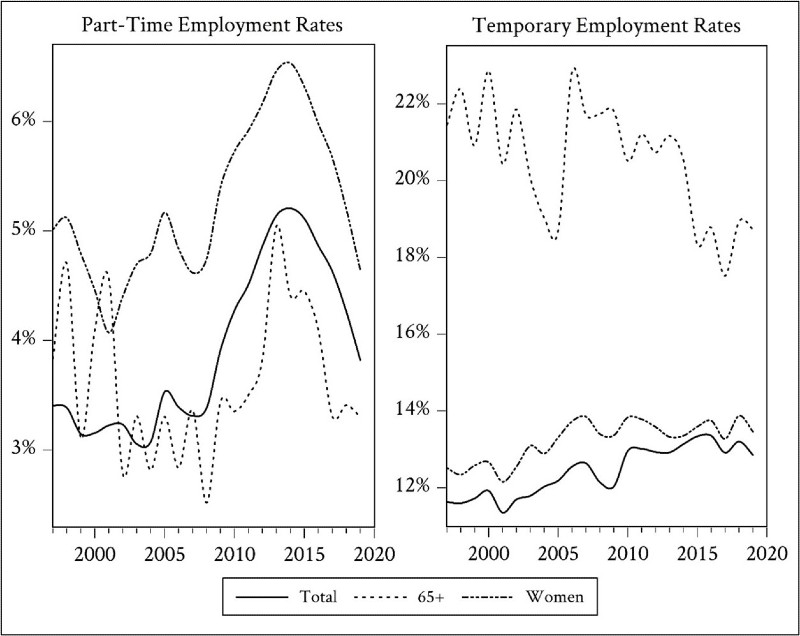

Notes: Temporary employment (% of dependent employment) includes wage and salary workers whose job has a pre-determined termination date. Part-time employment (% Employment; involuntary) refers to people in employment (employees and self-employed) who work less than 30 hours per week. The denominator for each variable is the employment level for each sub-group. Both variables are means of the full sample of OECD economies. (Source: OECD)

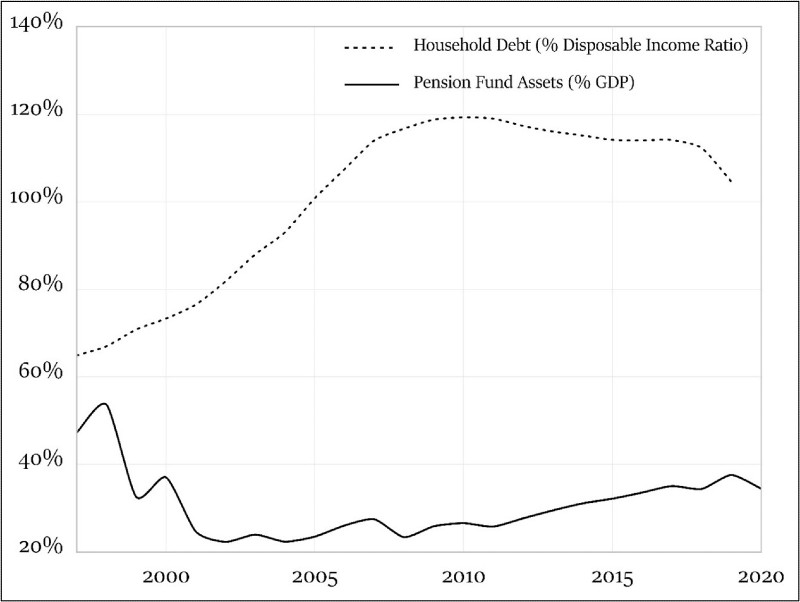

Notes: Household Debt is the sum of loans (primarily mortgage loans and consumer credit) and other accounts payable by households (% disposable income). Pension Fund Assets are the sum of assets bought with the contributions to a pension plan for the exclusive purpose of financing pension plan benefits (% GDP). Both variables are means of the full sample of OECD economies. (Source: OECD)

Further information

Gouzoulis, G., Iliopoulos, P., and Galanis, G. (2022). ‘Financialisation and the Rise of Atypical Work.’ British Journal of Industrial Relations, https://doi.org/10.1111/bjir.12701.

Authors

Dr Giorgos Gouzoulis (University of Bristol); Dr Panagiotis (Takis) Iliopoulos (KU Leuven); Dr Giorgos Galanis (Queen Mary University of London)

Policy Briefing 119: Oct 2022

Tackling precarious work through financial regulation and private debt relief (PDF, 4,550kB)